Together with, the inability to market the property because of a job import or relocation to a different area does not meet the requirements as the a keen extenuating circumstances.

Immediately after a foreclosure, it is possible to typically need to hold off two years to get a Va-protected home loan, possibly reduced if the experience are away from manage. Although not, sometimes, you may need to await three. Like, for many who cure the FHA-insured the place to find foreclosure, you may have to hold off 36 months prior to getting a Virtual assistant-protected home loan.

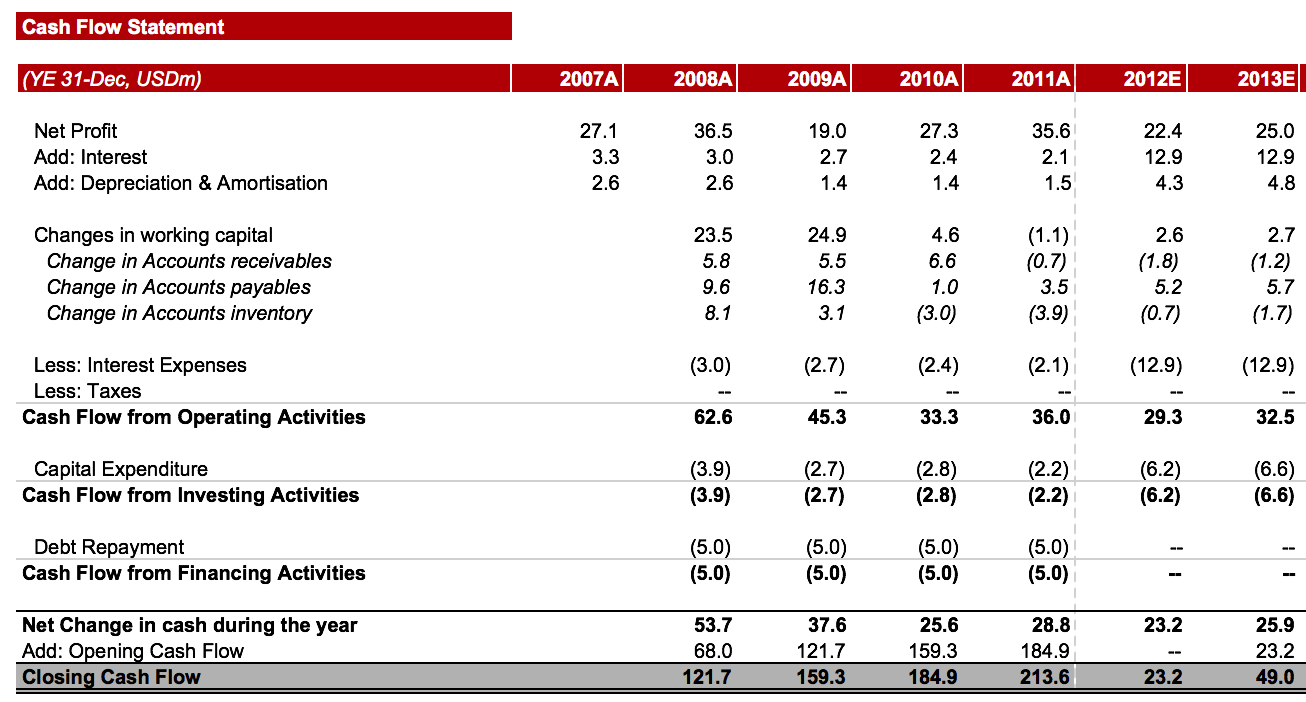

Page Contents

Prepared Period with other Types of Funds Just after Property foreclosure

For the majority of other sorts of financing, particularly subprime financing, waiting periods may vary. Of numerous commonly given that easy as for FHA-covered and you can Va-protected finance. New wishing several months vary of a couple of to eight age otherwise lengthened.

Particular lenders might shorten the fresh new article-foreclosure prepared months, provided you make more substantial deposit-eg, 25% or even more-and agree to spend a top interest.

Exactly how Your credit score Impacts Your odds of Bringing a separate Real estate loan

Notwithstanding the brand new prepared symptoms, you have to introduce good credit following a foreclosure before you can will get another home loan; your credit rating must meet the lender’s limited conditions. Plus when you can rating another type of home loan having a somewhat lower credit score, you might have to create more substantial deposit or shell out a higher rate of interest.

And this Credit rating Is used having Mortgage loans?

Fico scores are often used in the mortgage-financing business. Score fundamentally cover anything from 3 hundred to 850. FICO has many additional scoring habits, including FICO, FICO 8, and you may FICO nine. Another person’s score always varies with regards to the model always write it and you can which credit scoring agencies considering the underlying borrowing declaration.

For around 20 years, Federal national mortgage association and you will Freddie Mac requisite loan providers to make use of the brand new “Classic FICO” credit score to check on borrowers’ borrowing. With the , brand new Government Houses Fund Department (FHFA) launched it do fundamentally need loan providers to deliver each other FICO 10T and you can VantageScore cuatro.0 fico scores with each loan sold so you can Federal national mortgage association and you can Freddie Mac computer. (The latest FHFA is the authorities institution you to oversees Federal national mortgage association and Freddie Mac computer.) It change can happen a little while for the 2025.

FICO 10T and VantageScore 4.0 thought different kinds of fee histories having consumers than Classic FICO. For example, when available, they are rent, utilities, and telecommunications payments into the figuring ratings.

Needed Fico scores for brand new Mortgages

As of 2024, Fannie mae essentially personal loan with no monthly fee need consumers to own a credit history of 620 or 640, depending on the situation. According to the products, Freddie Mac computer requires a rating away from 620 otherwise 660 to have good single-loved ones number 1 house. Needless to say, loan providers possess requirements that will be stricter.

A keen FHA-covered loan with a low down-payment (step 3.5%) requires a rating regarding 580. You could potentially however qualify for an FHA-covered mortgage that have an excellent FICO score regarding five hundred to 579, but rather of developing an excellent 3.5% advance payment, your own deposit might possibly be higher, at least 10%. However, since the a foreclosures might cause your FICO rating to decrease of the one hundred circumstances or more, possibly lower than five hundred, you do not qualify for a mortgage, despite this new waiting months expires.

The Virtual assistant will not put a minimum credit history requisite. It needs lenders to review the whole loan character. O ften, loan providers want a good FICO credit score more than 620. Some loan providers allow lower scores, however, individuals need certainly to go through a lot more analysis and meet almost every other standards to help you score financing.

Just how to Re-Establish Good credit Just after a foreclosures

- spend your debts on time, constantly

- maintain your credit membership balances reduced