Page Contents

Home Security Credit lines (HELOC)

Household guarantee credit lines (HELOC) provide individuals to your liberty to access fund doing a specified borrowing limit, exactly like a regular line of credit. That have a great HELOC, you might obtain, pay-off, and you may borrow once again as needed .

The financing limit to have a great HELOC is normally determined by a beneficial percentage of your own house’s appraised worth, without any a great home loan balance. The interest rates towards the an effective HELOC are varying, meaning they can change over the years. This will be beneficial if interest levels are reduced, but it is vital that you be ready for potential increases on the coming.

One of the benefits of an excellent HELOC is you just shell out desire toward count you borrow, maybe not the complete credit limit. This provides you deeper control over their borrowing can cost you. However, it is imperative to build timely money to stop accumulating excess financial obligation and you can prospective property foreclosure dangers.

Reverse Mortgages

Contrary mortgages is an alternative choice for residents to access their property guarantee. This type of mortgage allows people aged 55 otherwise more mature in order to use around a specific portion of the home’s appraised really worth. The fresh lent number, also amassed notice, is generally paid back in the event the homeowner sells the home otherwise through to its passing.

What kits opposite mortgages apart is that consumers don’t need and also make regular monthly payments. Rather, desire into the loan adds up over the years, improving the total mortgage equilibrium. This really is very theraputic for retired people who has got the websites tight budget however, want to access the value of their residence.

You will need to very carefully look at the ramifications of a face-to-face mortgage. Although it can provide economic flexibility, it also function probably decreasing the heredity that can be passed to family. Before deciding into the a contrary home loan, you might want to look for top-notch financial pointers to fully comprehend the long-term impact.

Both household security personal lines of credit (HELOC) and you may reverse mortgage loans promote choices to conventional house collateral money, providing home owners with various a means to supply the newest collateral within their homes. Knowing the benefits, risks, and you may qualifications conditions ones choice is very important to make an enthusiastic informed choice in the and that road is best for your unique financial disease.

Qualifying getting a property Equity Loan

Being qualified to have property guarantee financing need appointment specific requirements lay by lenders. Important aspects one loan providers envision whenever comparing eligibility getting a home collateral loan include credit rating, money, and loans-to-money proportion.

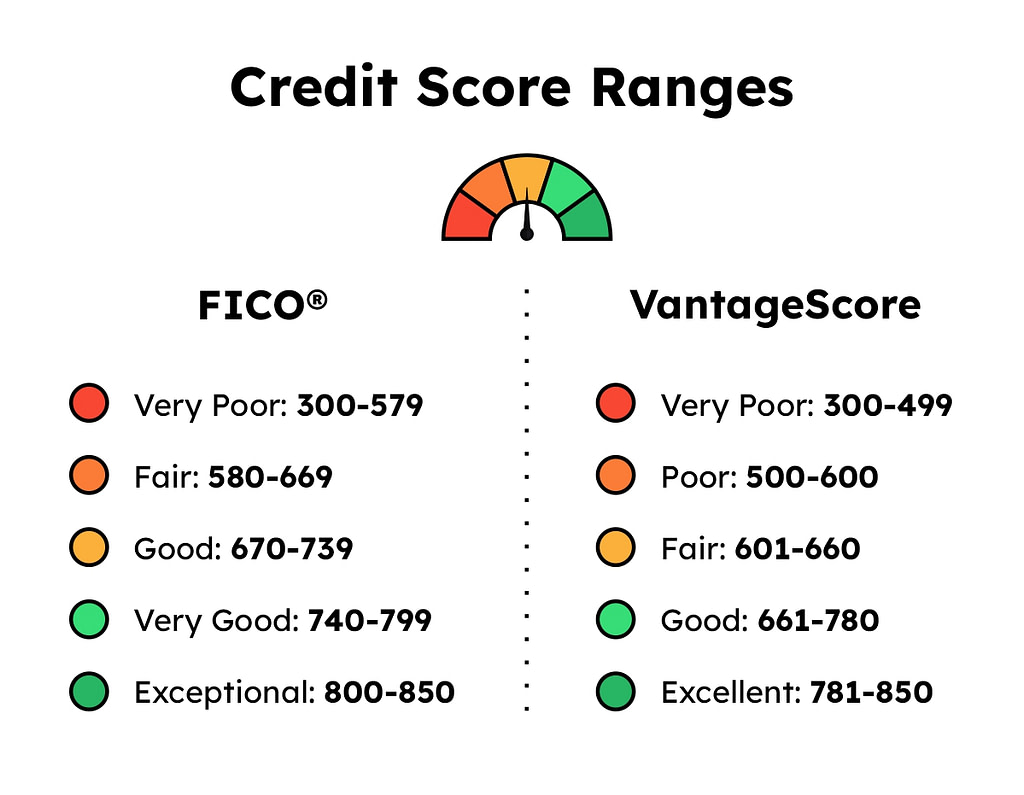

Credit rating and you may Qualifications

Loan providers generally determine good borrower’s creditworthiness by the evaluating their credit score. A higher credit history shows in charge monetary decisions and boosts the likelihood of qualifying having a house equity loan. While credit score criteria ong lenders, good credit can be considered to be over 670.

Maintaining an effective credit history through fast money to the existing costs, remaining credit utilization reduced, and avoiding a lot of financial obligation can help raise credit ratings. It’s important to comment and you may understand your credit score, dealing with any problems otherwise discrepancies, before you apply to possess a property collateral mortgage.

Earnings and you will Financial obligation-to-Money Ratio

Income is another essential factor that loan providers check when determining qualifications to own a property security loan. Loan providers want to make certain that individuals has actually a reliable and sufficient income in order to satisfy the financing debt. They often look at the borrower’s personal debt-to-earnings (DTI) ratio, and that compares the latest borrower’s monthly loans money on the month-to-month money.

A lower DTI proportion is good as it implies a lesser financial burden. Loan providers essentially like an effective DTI proportion less than 43%, whether or not particular criteria can differ. To help you estimate their DTI ratio, add up your month-to-month personal debt repayments (particularly financial, handmade cards, and you will financing) and you may separate they by the terrible month-to-month earnings. Multiply the end result of the 100 to obtain the commission.