Loan-to-really worth proportion is simply an assessment away from everything you nonetheless owe with the mortgage on the property’s appraised really worth. A lowered LTV increases your odds of qualifying to own an excellent home collateral financing. Moreover it identifies the maximum amount that you will be capable use with a property collateral loan otherwise HELOC.

You can calculate your current LTV as well as how much you might be qualified in order to use with these domestic equity loan calculator. That may make you a much better concept of what you are likely so you’re able to be eligible for.

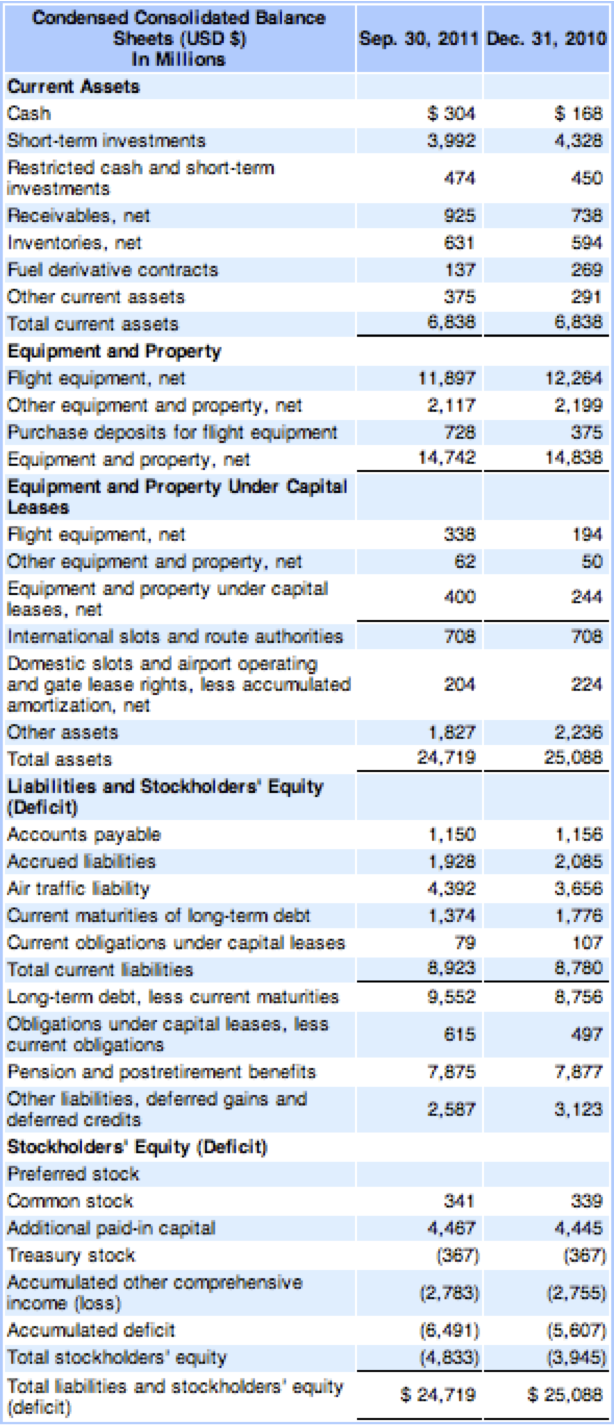

Page Contents

Debt-to-income ratio

As stated inside our dialogue of income, lenders will also check your obligations-to-earnings ratio. Your debt-to-income proportion shows the newest portion of your terrible month-to-month earnings you to would go to obligations payment every month.

Lenders calculate DTI based on your debt burden as well as your asked commission to the house guarantee loan otherwise HELOC.

A reduced loans-to-earnings proportion is the most suitable, because means that you have sufficient earnings to satisfy every of one’s debt obligations. Increased DTI, in addition, you’ll place you on greater risk out-of default if you’re incapable to keep track their individuals personal debt payments.

That’s where the prerequisites may differ a small with the domestic collateral loan as well as the personal line of credit. That have house equity financing, loan providers generally get a hold of a great DTI proportion away from 43% otherwise below. But with HELOCs, specific loan providers get enable it to be an optimum DTI proportion as high as 50%.

In the event your DTI is close to or on restrict to own a property equity financing otherwise HELOC, you’ll find some things you can certainly do to carry they down. First, you could find a method to raise your money. So you might score a member-day jobs, improve period at the job if you’re paid hourly, otherwise begin an area hustle.

Another possibility will be to lower some of your obligations. If that’s possible can depend on the income and just what you may have for the offers. Nevertheless way more obligations you could potentially get rid of, the greater their recognition chances is whenever applying for family guarantee activities.

How can home collateral mortgage conditions are different from the financial?

Household collateral financing and HELOCs are subject to underwriting hence procedure, and conditions having recognition, will vary for each and every lender. All bank has its own laws set up to possess computing exposure, gauging the chances of default, and you can qualifying individuals to have funds or lines of credit.

Loan providers normally, however, provide some direction off things such as credit scores and you will limit mortgage amounts. You could potentially constantly find these records to your lender’s webpages or of the getting in touch with him or her.

Comparing household equity tool criteria at different lenders can give you a sense of for which you could have a far greater likelihood of providing recognized. And continue maintaining in your mind one borrowing unions, antique finance companies, an internet-based banking institutions can also be all of the handle household equity activities in a different way.

Borrowing connection home guarantee mortgage conditions

A cards partnership is actually a no more-for-earnings registration company that works on the advantage of their users, in the place of concentrating on the bottom line. Borrowing unions are apt to have more freedom within their lending recommendations than simply banking companies as they are able to deal with an advanced level from risk.

You will need to satisfy membership criteria to try to get a house collateral mortgage otherwise press the site HELOC. Membership requirements can differ by the borrowing union and can even feel mainly based on at the office, check out college or university, live, or worship.

Conventional financial HELOC standards

Brick-and-mortar banking institutions become seemingly rigorous regarding their direction and underwriting criteria when compared with borrowing from the bank unions. You may want getting a high credit history to help you be considered, such as. Or you may prefer to convey more equity yourself to qualify.